|

Dear Friends and

Neighbors,

Happy Summer Solstice!

Anchorage received 19

hours and 21 minutes of daylight.

Photo: Gold Creek, Juneau’s source

of drinking water, coming out of Silver Bow Basin. At headwaters

was the 1880s Alaska-Juneau Gold Mining Company operations.

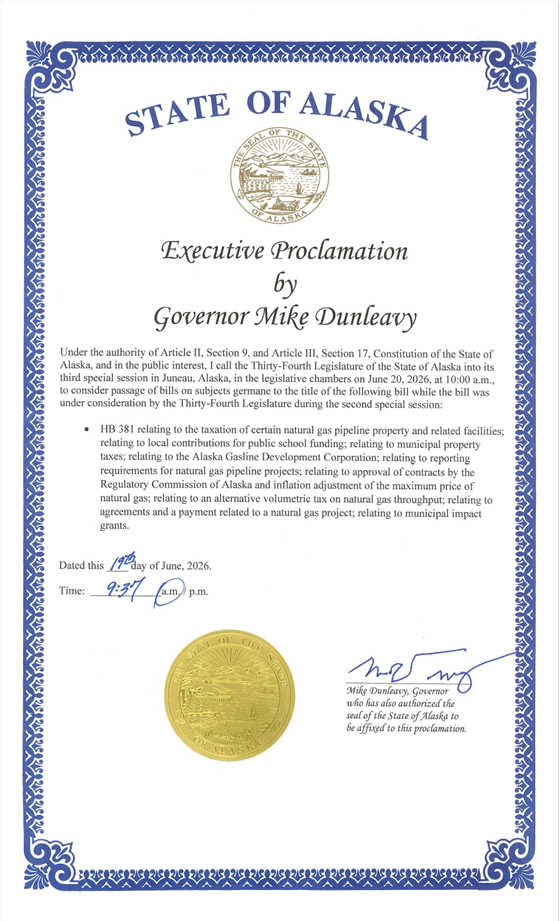

THIRD Special Session -

Day 3

Gas Pipeline is the only

topic.

Why a THIRD SS? The

Governor didn't like the changes that the Senate made in the

policy.

Gas Pipeline Bill Passed the Senate

The Governor was unhappy

with the Senate adjustments made in his Gas Pipeline bill.

"S-Corp tax"

Fundamental to remember:

Alaska has no personal income tax.

Only

"C-corporations" pay corporate income tax in Alaska.

There are over 12,000

"S-corporations in Alaska.

The S-Corp tax is more technically called

Subchapter S Tax in the Internal Revenue Code –

· Glenfarne falls under this federal tax

category. This category is taxed through the personal income

taxes paid by citizens who own the private Subchapter S

company. These eligible domestic corporations or LLCs to pass their

income, losses, deductions, and credits directly to company owners.

The business itself does not pay federal income tax.

· Different from Subchapter C of the Internal Revenue

Code. These C-Corporations are any business entity taxed as a

distinct, separate legal entity from its owners. The company pays

the taxes on net profits. It is the default tax classification for

state-registered corporations.

· Exxon and Conoco, who produce the gas on the

North Slope, are C-corporations. They

will sell the gas to Glenfarne-owned Gas Treatment Plant and Gas

Pipeline.

· Baker Hughes, a C-corporation, is a

construction contractor hired by Glenfarne to

manage and build many portions of the Gas Project.

· Alaska Airlines, a C-corporation, will

transport 22-68% of the out-of-state workforce needed as they work their shifts on this project.

· (This “22-68%” is the number given in the

Federal Energy Regulatory Commission (FERC) EIS submitted by AGDC

and Glenfarne. See page 4-624 and 4-626 of EIS (Final

Environmental Impact Statement-Alaska LNG Project | Federal Energy

Regulatory Commission).

Alaska Airlines,

BakerHughes, Exxon, and Conoco will all pay federal corporate tax

and state corporate tax.

Why should Glenfarne be

exempted from Alaska State Corporate Income Tax?

· Alaska Department of Revenue projects that the

Subchapter S policy contained in the Gas Pipeline bill would result

in about $100 million/year in 2033, and up to nearly $600

million/year by 2052 in state revenue from just Glenfarne

alone. Reference

5-14-2026, Senate Resources, slide 33.

· Amendment: S-corporation

tax, proposed in the Gas Pipeline bill, would begin the tax at NET Profits of

$1-2 Million, tax of 5% of profits; $2-3 Million: 6% tax; $3-4

Million: 7% tax; $4-5 Million 8% tax; more than $5 Million: 9.4%

tax.

· There are other S Corporations be included in

this tax update. It will apply to companies who produce or

transport oil or gas.

Other SENATE CHANGES MADE in the Gas Pipeline

bill

· Union contracts honored as project

labor agreement, prevailing wage, and apprenticeship utilization

requirements

· Inflation

in the pipeline taxes would be EQUAL to the inflation rate in the cost of gas paid by Alaskans would

pay. Original version from the Governor had Alaskans paying FULL

INFLATION, while Glenfarne's taxes were half of that inflation

rate.

· Prohibit Alaskans

paying Glenfarne back for FAILURE OR ABANDONING THE PROJECT.

· Prohibit Alaskans

paying for Glenfarne's COST OVERRUNS on the project.

· Prohibit Glenfarne

entering into a legal relationship with a foreign entity, either

directly or indirectly through another person or entity without notifying the Legislature.

On

page 27 of the bill the Senate version required that Glenfarne reach

Final Investment Decision by January 1, 2028. This means they

would have recruited the funding commitments from investors.

The Senate version

required that Glenfarne complete construction of the gas

pipeline to the SouthCentral gas system by December 31, 2032.

This would be before the Cook Inlet gas contracts expire in 2033.

We were not successful in

correcting all the problems that the Senate Majority identified in

the bill.

Here

are all the amendments offered on June 19.

However, with the

amendments listed above, I was comfortable voting in favor of the

bill.

It passed the Senate 12-8.

There have been rallies

claiming that this pipeline would ensure "cheap gas for

Alaskans".

Nothing will do that.

In fact...

Alaska

Department of Revenue says: The Revenue impact of

this bill is indeterminate. The revenue impact could be positive or

negative and could impact state finances by hundreds of million of

dollars, or more, per year. Key uncertainties include the impact of

this billon whether the Alaska LG project moves forward, detailed

final project cost and timing, timing for when the temporary tax

abatement ends and the AVT applies, component capital expenditure

weights, and completed construction costs. (Costs estimated for

Dept of Revenue: more than $1 million/year)

Bills that pass into law without the

Governor's signature

HB

184 AIDEA: WORKFORCE HOUSING

DEV.; MUNI TAX

HB

239 CRIME/CNTRL SUBST/ADDRESS

CONFIDENTIALITY

HB

27 MEDICAL MAJOR

EMERGENCIES; CPR CURRICULUM

HB

363 ALCOHOL: PATRIOTIC ORGS;

CLUB LICENSES

HB

28 EDU:

SCHOOLS/TEACHERS/SCHOOL BD/LOAN PRGM

HB

117 ELEC MONITOR TRAWL

FISHERY/SET NET PERMIT

SB

104 VEHICLES/BOATS: TRANSFER

ON DEATH TITLE

SB

146 REAA & SMALL MUNI

FUND: MT. EDGECUMBE

SB

164 ELIMINATE TAX DISCOUNTS

SB

167 PFD ELIGIBILITY; PFD FOR

OVERTURN CONVIC.

SB

178 EXPAND EARLY INTERVENTION

SERVICES

SB

187 SCHOOL NUTRITION/MEAL:

PROHIBIT FOOD DYES

SB

23 CIVICS EDUCATION

SB

272 HEALTH INFORMATION

EXCHANGE

SB

79 PAYMENT OF WAGES; PAYROLL

CARD ACCOUNT

SB

89 PHYSICIAN ASSISTANT SCOPE

OF PRACTICE

Resolutions

SJR

20 CLEAN UP MARINE DEBRIS

SR

4 250TH

ANNIVERSARY OF UNITED STATES

Items in this Newsletter:

· Special Session #3 Proclamation

· Gas Pipeline Finance meeting

· Oil and Gas Pipeline Topics with Current

Topics, Stuff I Found Interesting, Education, Politics, Healthcare

· Resource Values, Permanent Fund Data

|